Fundamentals of CLO Collateral and Structure

Collateralized loan obligations are securitizations typically backed by pools of corporate loans and other corporate-credit related assets.

- Underlying loans are typically senior secured, floating rate corporate loans

- The vast majority of loans carry public credit ratings from major rating agencies such as S&P, Moody’s, and Fitch

CLOs receive principal and interest cash flows from their underlying assets and typically distribute them quarterly.

- Senior debt tranches are paid first, then mezzanine debt tranches, then equity tranches

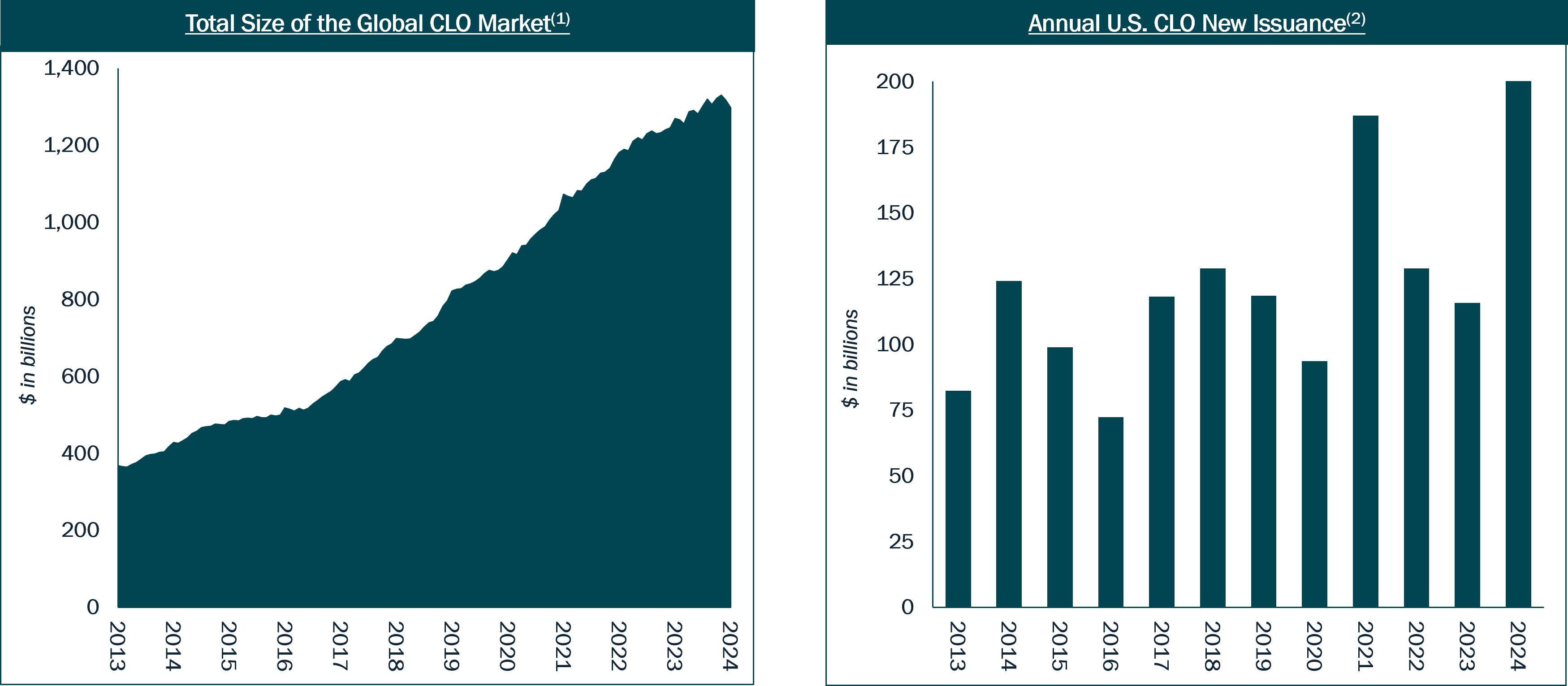

CLO Market Overview

Growing Asset Class with Improving Liquidity and Scalability

Global CLO market has nearly doubled in size to $1.3 trillion(1) since 2018 and is now the largest asset class in the private-label securitized products universe.

We believe this rapid growth has meaningfully improved availability and liquidity of CLO mezzanine debt and equity in the secondary market.

CLO market growth has significantly expanded the investment opportunity set, especially as the spectrum of seasoned investment profiles continues to broaden.

Attractive Investment Opportunities

We believe that many parts of the CLO market remain highly inefficient, with much of the increased participation in the space coming from investors focused on adding the most liquid and standardized profiles.

We believe attractive investment opportunities exist for sophisticated institutional investors who are able to conduct thorough analysis of the documents, structures, and underlying corporate borrowers in less standardized CLO investment profiles.

We believe dispersion in CLO collateral performance going forward should continue to provide ample ongoing investment opportunities.

A CLO-focused closed-end fund provides individual investors access to a differentiated investment strategy otherwise limited to the institutional market.

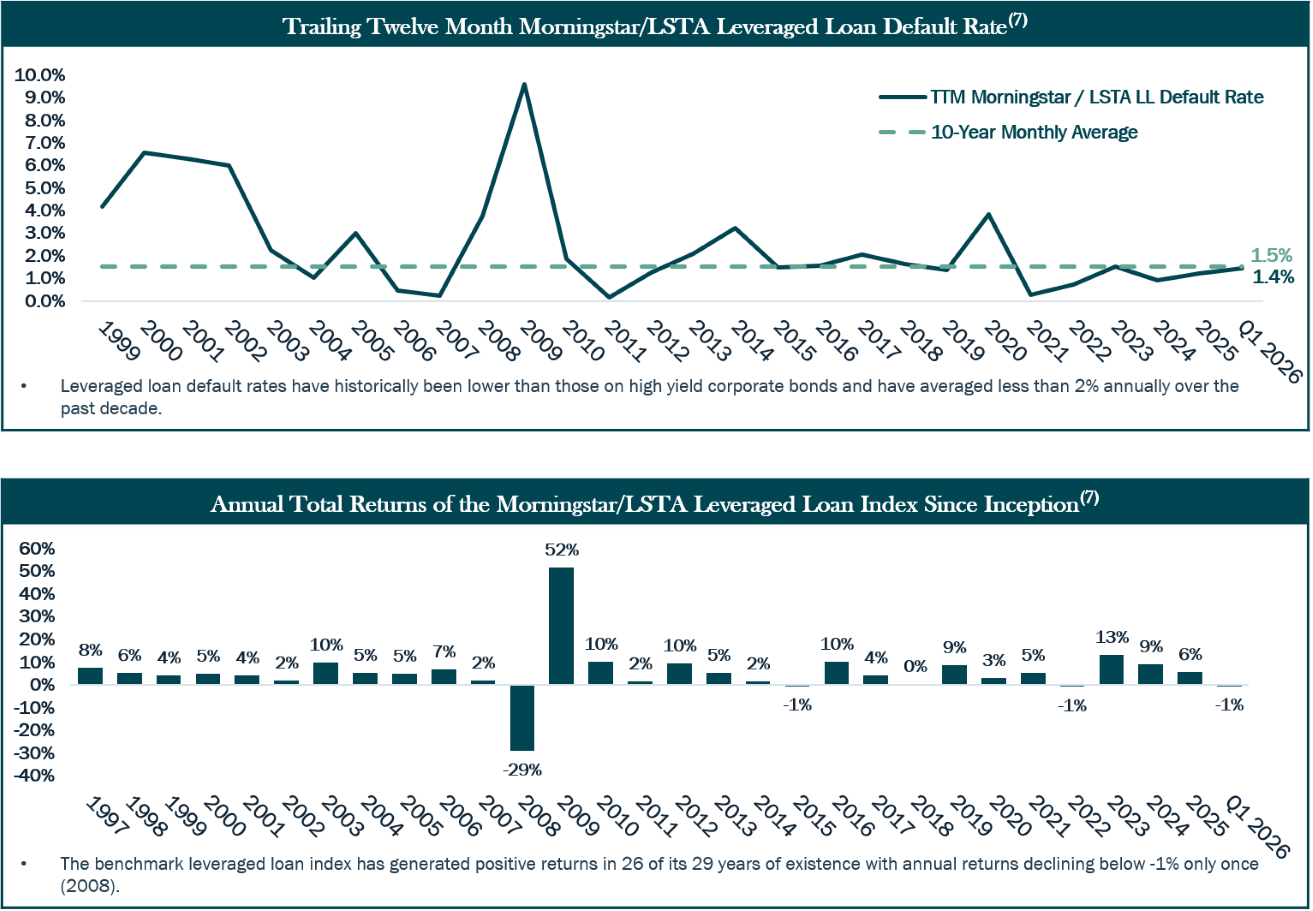

CLOs have historically experienced better credit performance than the benchmark leveraged loan index

Historically, CLO debt tranches have demonstrated resiliency to corporate defaults due to structural features that preserve cash flows in times of stress, such as:

- Credit enhancements in the form of subordinate securities and overcollateralization

- Floating rate notes with excess spread

- Deal triggers that divert excess interest to protect debt tranches

CLOs are typically actively managed vehicles, allowing collateral managers to rotate the assets in their portfolios to react to changing market conditions and credit events.

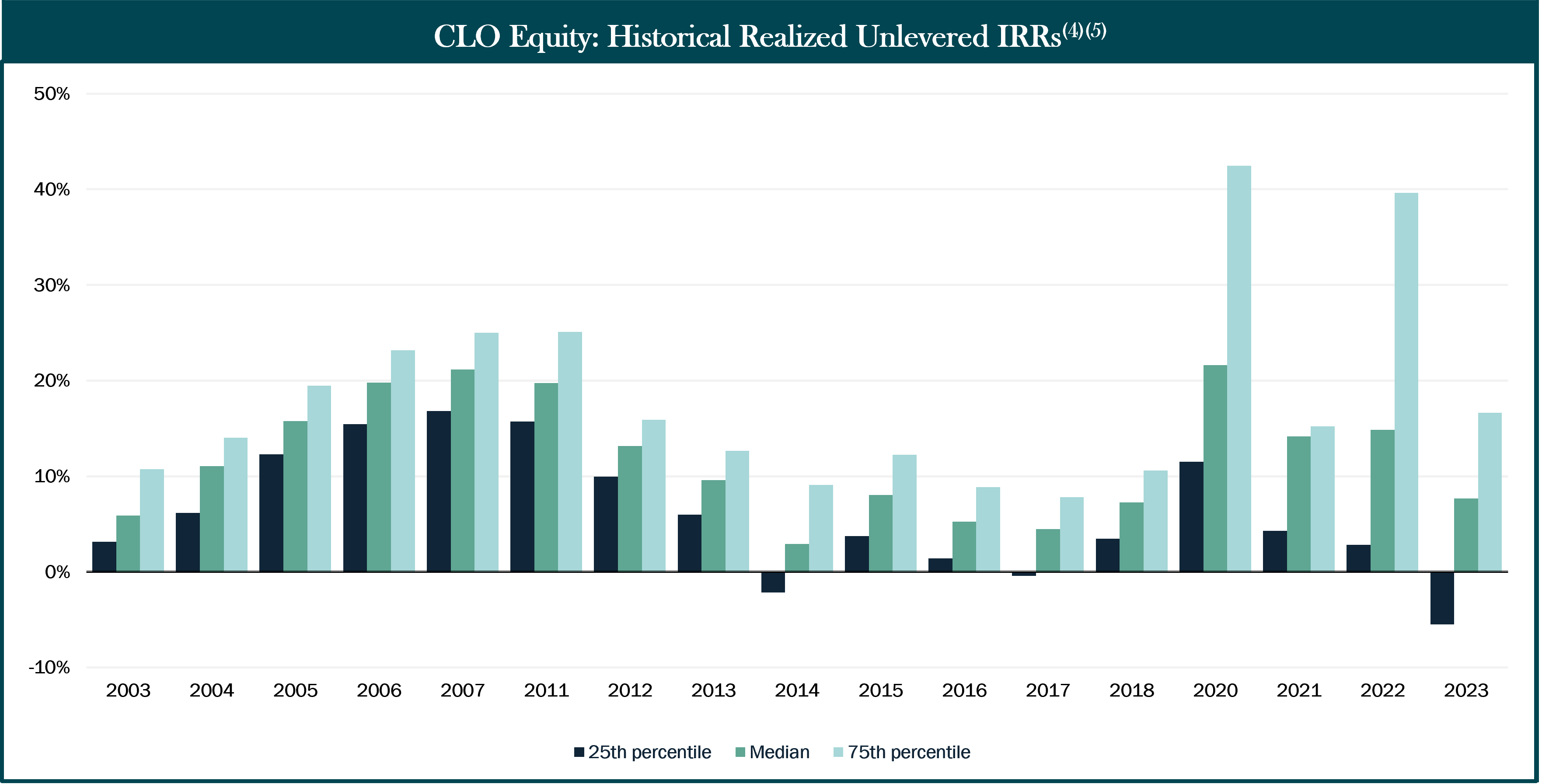

CLO Equity Overview(4)

CLO equity tranches can offer an attractive return profile for investors, including strong current carry.

The chart below shows historical realized unlevered internal rates of return ("IRRs") by CLO equity vintage, assuming each equity investment was purchased at new issuance and held to the conclusion of each CLO.

- IRRs may be further enhanced by investing in CLO equity at higher yields in secondary markets and/or by actively trading, both of which are core tenets of Ellington’s strategy.

CLO equity vintages between 2003 – 2023 have generated a median unlevered IRR of ~11%, assuming each investment was held from new issuance to deal conclusion.(5)

- However, performance has varied widely between CLOs, and we believe the complexity of the asset class requires strong analytics and underwriting capabilities to determine which investments may under- or out-perform.

CLO Mezzanine Debt Overview

CLO mezzanine debt tranches offer several advantages over other corporate credit sectors including:

- Attractive yield profiles relative to similarly-rated corporate credit investments

- Credit enhancement, allowing structures to withstand significant loss levels

From 2010 through 2024, S&P Global Ratings rated nearly 19,000 tranches and found an average annual default rate of only 0.04% for CLO BB tranches and 0.16% for CLO B tranches.

- These annual average default rates are well below the default rates for similarly rated corporate bonds, as depicted below.

Leveraged Loan Performance and Resiliency Over Time

Past performance is not necessarily indicative of future results

- Source: BofA Global Research as of December 31, 2024.

- Source: Pitchbook | LCD as of December 31, 2024.

- Source: J.P. Morgan.

- Past performance is not necessarily indicative of future results. The table is provided for illustrative purposes only. The actual performance of EARN's portfolio may differ from the performance of the CLO equity market as presented. The performance of the CLO equity market does not reflect management fees, performance fees, and other expenses incurred by the fund, which will reduce the returns of EARN's portfolio. Deal vintages from 2024 and later are excluded from the chart due to the limited sample size of fully redeemed transactions from those vintages.

- Source: BofA Global Research as of March 31, 2026.

- Source: S&P Global Ratings Credit Research & Insights and S&P Global Market Intelligence's CreditProSource: BofA Global Research. CLO default data is through May 2025 and corporate default data is through December 2024.

- Source: LCD / Morningstar LSTA Leveraged Loan Index as of March 31, 2026. Past performance is not indicative of future results.

Cautionary Statement Regarding Forward-Looking Statements

This webpage contains forward-looking statements within the meaning of the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Forward-looking statements are not historical in nature and can be identified by words such as "anticipate," "estimate," "will," "should," "may," "expect," "project," "believe," "intend," "seek," "plan" and similar expressions or their negative forms, or by references to strategy, plans, or intentions. Forward-looking statements are based on our beliefs, assumptions and expectations of our future operations, business strategies, performance, financial condition, liquidity and prospects, taking into account information currently available to us. These beliefs, assumptions, and expectations are subject to numerous risks and uncertainties and can change as a result of many possible events or factors, not all of which are known to us. If a change occurs, our business, financial condition, liquidity, results of operations and strategies may vary materially from those expressed or implied in our forward-looking statements. The following factors are examples of those that could cause actual results to vary from those stated or implied by our forward-looking statements: changes in interest rates and the market value of our investments, market volatility, changes in the default rates on corporate loans, our ability to borrow to finance our assets, changes in government regulations affecting our business, a deterioration in the market for collateralized loan obligations, our ability to adapt to the new regulatory regime associated with our conversion to a closed-end fund/RIC, potential business disruption related to our conversion to a closed-end fund/RIC, ability to achieve the anticipated benefits of our conversion to a closed-end fund/RIC, the acceptance by the IRS of the proposed change to our tax year, and other changes in market conditions and economic trends, such as changes to fiscal or monetary policy, heightened inflation, increased tariffs, slower growth or recession, and currency fluctuations. Furthermore, as stated above, forward-looking statements are subject to numerous risks and uncertainties, including, among other things, those described under the heading “Risk Factors” in our Registration Statement on Form N-2, which can be accessed through the link to our SEC filings under "For Investors" on our website (at www.ellingtoncredit.com) or at the SEC's website (www.sec.gov). Other risks, uncertainties, and factors that could cause actual results to differ materially from those projected or implied may be described from time to time in reports we file with the SEC, and is not possible for us to predict or identify them all. We undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise. This webpage and the information contained herein do not constitute an offer of any securities or solicitation of an offer to purchase securities.